Barchart announced that U.S. banks still face $329 billion in unrealized losses. FDIC data revealed that U.S. banks reduced their unrealized losses from $361 billion in Q2 2023 to $329 billion in Q3.

FDIC argued that banks are progressing with interest rates but are still far from being clear. The agency added that Longer-term interest rates, particularly the 30-year mortgage and the 10-year Treasury rates, declined in Q3, which increased the value of securities reported by banks.

U.S. banks face $329 billion in unrealized losses in Q3

🚨🇺🇸BANKS STILL FACING $329 BILLION IN UNREALIZED LOSSES

New FDIC data shows U.S. banks reduced their unrealized losses from $361 billion in Q2 to $329 billion in Q3.

It’s an improvement, but $329 billion is still a massive number.

With rising interest rates and market… pic.twitter.com/izrFaIzXdU

— Mario Nawfal (@MarioNawfal) December 14, 2024

The Federal Deposit Insurance Corporation (FDIC) revealed in its third-quarter performance results that FDIC-insured institutions faced $329 billion in unrealized losses.

According to the insurance corporation, the net interest margin increased for all banks. The banking industry also reported an increase in loan yields that exceeded the increase in the cost of deposits for the first time since Q2 2023. The surge in loan yields resulted in an increase in banks’ net interest margin by 7 basis points to 3.23%, which reversed a Q3 trend where the industry’s margin fell by 14 basis points.

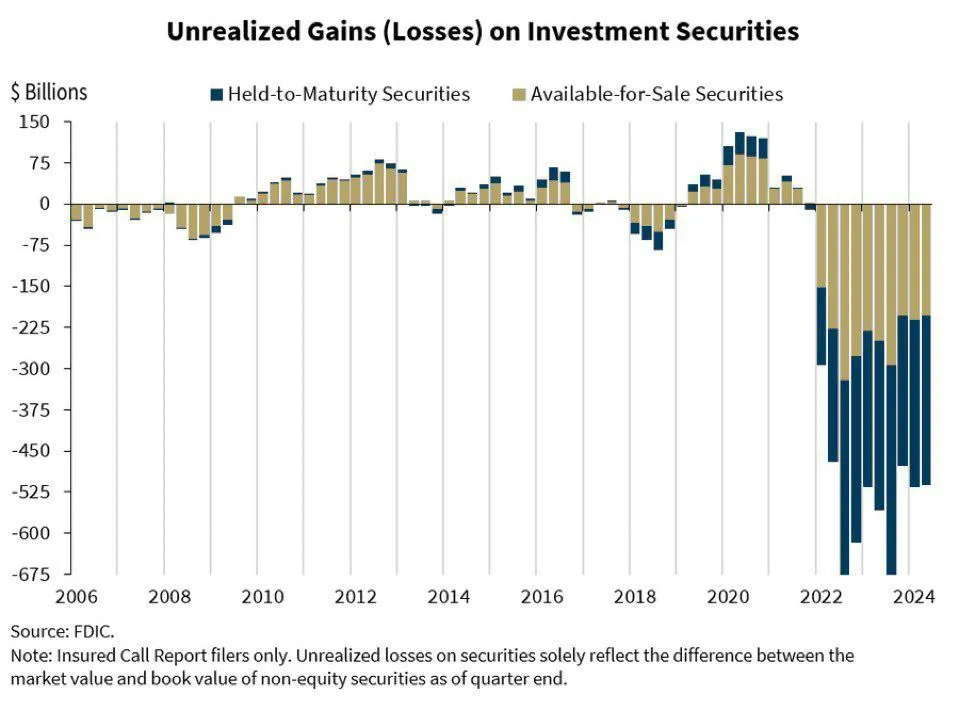

Unrealized losses on available-for-sale and held-to-maturity securities declined by $149 billion to $364 billion in Q3. The government agency revealed that longer-term interest rates, in particular the 30-year mortgage and the 10-year Treasury rates, declined in Q3, which increased the value of securities reported by banks. The increase in longer-term interest rates after the end of the third quarter reduced the unrealized losses to $329 billion.

The banking industry’s net interest income and net interest margin increased in Q3, although asset quality metrics deteriorated. However, they remained favorable despite continued weakness in several loan portfolios, which the FDIC said it would monitor closely.

The agency revealed that the banking industry’s net income of $65.4 billion in Q3 was a decrease of $6.2 billion (8.6%) from Q2 due to the absence of one-time gains on equity security transactions of ~$10 billion last quarter. The banking industry also reported an increase in net interest income of $4.5 billion in Q3 that partially offset the absence of those gains.

FDIC believes U.S. banks still face downside risks

The banking industry’s total loans increased by $77 billion (0.6%) in Q3, with the largest portfolio increase reported in loans to non-depository financial institutions. The industry’s annual rate of loan growth also increased to 2.2% in Q3.

Domestic deposits increased in Q3 by $195 billion (1.1%), and the FDIC highlighted that estimated uninsured deposits drove the increase. Brokered deposits also declined $47 billion (3.6%) from Q2, which the agency confirmed contributed to the lack of growth in insured deposits.

According to the FDIC report, the Deposit Insurance Fund (DIF) balance also increased by $3.9 billion from the end of Q2 to $133.1 billion on September 30. The insurance firm also maintained that the reserve ratio remained on track at 1.25% in Q3 and expected it to reach the 1.35% minimum reserve ratio by the end of 2026.

The number of banks on the Problem Bank List, which encompasses banks that have a

According to the FDIC, the number of banks with a CAMELS composite rating of “4” or “5” increased by two in Q3 to 68. The agency also revealed that the total assets held by problem banks increased by $4 billion to $87 billion during the quarter.

The report also highlighted that weak demand for office space continued to soften property value, and higher interest rates over the past years affected the repayment and refinancing of office and other CRE borrowers. The banking industry’s past-due rate for non-owner-occupied CRE loans increased in Q3.

The FDIC maintained that the banking industry continued to show resilience in Q3 but still faced significant downside risks from the continued effects of inflation, volatility in market interest rates, and geopolitical uncertainty. The agency believes these issues could cause credit quality, earnings, and liquidity challenges for the industry. The firm added that weaknesses in certain loan portfolios, particularly office properties, credit cards, auto, and multifamily housing loans, continued to warrant close monitoring.

From Zero to Web3 Pro: Your 90-Day Career Launch Plan