Do you want a blockchain app that redefines how your business operates? Blockchain technology now revolutionizes industries from finance to healthcare, and its potential for innovation remains undeniable. However, a successful blockchain application requires more than mere knowledge of its benefits—it calls for a structured approach. In this guide, we’ll outline the steps to build a blockchain app, including how to choose the right platform, deal with common challenges, and create an application that aligns with industry standards. By the end, you hold a roadmap that transforms your blockchain vision into reality.

Key benefits of blockchain applications in development

Blockchain apps, often referred to as decentralized applications (DApps), are built on blockchain technology to use its distributed and secure infrastructure. Unlike traditional applications that rely on centralized servers for data storage and processing, blockchain apps operate on a peer-to-peer network. These applications form the foundation for financial software development services and other use cases. This approach provides transparency, security, and resilience, setting them apart as a revolutionary technological advancement.

Blockchain applications have gained attention due to their ability to address challenges related to data security and transparency. These benefits make blockchain a valuable tool across industries, from finance to healthcare and supply chain management. Below are the key advantages of blockchain applications:

Image created with napkin.ai

- Blockchain’s decentralized structure removes reliance on central authorities and lowers the risk of cyberattacks. Cryptographic algorithms preserve data integrity by linking each block to the previous one. This architecture makes blockchain applications highly resistant to tampering and provides a secure environment for sensitive transactions.

- Blockchain applications use distributed ledgers where all transactions are recorded identically across all nodes. This visibility eliminates the need for intermediaries and fosters trust and accountability. When businesses develop blockchain apps, transparency becomes a cornerstone that improves operations and customer confidence.

- With blockchain, every asset or transaction can be tracked throughout its lifecycle. Industries like supply chain and healthcare use this capability to provide compliance and authenticity.

- By automating processes with smart contracts, blockchain reduces the time and cost associated with traditional systems. These self-executing contracts streamline workflows, especially for businesses involved in crypto app development and financial operations. If you’re wondering how much does it typically cost to create a mobile app, these savings can offset development expenses.

- Smart contracts embedded in blockchain applications enforce terms and conditions automatically. This feature minimizes the need for third-party involvement, reduces disputes, and accelerates transaction processing.

The decision to develop blockchain applications is about staying competitive and using these distinct advantages to drive innovation and growth. With its unmatched security, transparency, and reliability, blockchain technology continues to redefine how businesses operate across industries.

How to develop a blockchain application

This section outlines a step-by-step approach to simplify the complexities of blockchain app development. Let’s begin with the foundational steps that set the stage for a successful development journey.

Step 1. Define your objectives

Identify the specific problem your blockchain application solves. Determine the purpose and value proposition of your app. For example, is it a cryptocurrency wallet, a decentralized finance (DeFi) platform, or a supply chain tracking solution? Clear objectives form the foundation for the entire development process.

Step 2. Conduct market research

Market research is needed to validate your idea and analyze the competitors. Examine existing blockchain solutions in your target industry to identify gaps and opportunities. Look for features that resonate with users and areas where competitors fall short. This insight can help you to refine your application and position it as a unique offering. Consider user expectations and trends to make sure your app aligns with market demands.

Step 3. Select the right blockchain platform

The platform you choose will impact the functionality and scalability of your application. For example, Ethereum is ideal for applications requiring smart contracts, while Hyperledger suits enterprise solutions. Each platform has unique characteristics, so evaluate your app’s requirements thoroughly to make an informed decision. Your choice will influence the technical capabilities of the app and the skill sets needed for development.

Step 4. Select the right blockchain platform

A well-planned blockchain architecture forms the backbone of your application. Begin by choosing the type of blockchain that best suits your app—public, private, hybrid, or consortium. For example, a public blockchain may fit an open financial app, while a private blockchain may better serve internal company use. Next, choose a consensus mechanism, such as Proof of Work (PoW) or Proof of Stake (PoS), which matches the desired level of transaction validation and scalability. Smart contracts must govern transactions accurately and securely.

Step 5. Develop the user interface (UI) and user experience (UX)

The user interface is where users interact with your application, which makes it an important component of the development process. Collaborate with designers to create a visually appealing, intuitive interface that guides users effortlessly through the app. A user-friendly design encourages adoption and builds trust. Consider the end-user’s journey and make sure the interface provides easy access to core features, regardless of the complexity of the underlying blockchain.

Step 6. Start the blockchain application development process

The development phase transforms your concept into a working application. Backend development focuses on building the blockchain logic, implementing smart contracts, and managing node interactions. Meanwhile, frontend development provides users with seamless access to the app’s features. Experienced developers integrate necessary APIs for functionalities like payment gateways and external data sources.

Step 7. Test the application

Testing is an indispensable part of blockchain application development. It verifies the app’s reliability, security, and performance. Functional tests confirm that the application performs as expected, while security tests identify vulnerabilities in the blockchain and smart contracts. Performance tests measure the app’s response under varying loads to confirm it can handle real-world usage. Rigorous testing helps detect and resolve issues early, reducing risks post-deployment.

Step 8. Deploy the application

Deployment marks the transition of your app from development to production. All features must be functional and comply with relevant platform guidelines, such as those of the App Store or Google Play, if your app targets mobile users. A smooth deployment process involves configuring the app’s infrastructure and addressing any last-minute adjustments to provide stability and user satisfaction.

Post-deployment, continuous monitoring is necessary to maintain your application’s functionality and security. Address issues quickly and update the app to accommodate new operating systems or frameworks. Regular maintenance also provides opportunities to introduce new features or improve existing ones, which keeps your app competitive and aligned with user needs. The success of your blockchain application doesn’t end with development—it requires promotion to reach its target audience. Marketing strategies such as SEO, paid advertising, and social media campaigns help generate awareness and drive user adoption.

Future trends in blockchain development

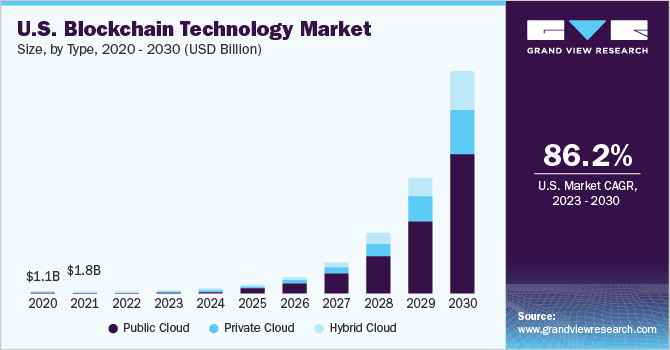

Blockchain technology continues to evolve, driving innovation across industries. According to a study, the global blockchain market, valued at $10.2 billion in 2022, is projected to grow at a compound annual growth rate (CAGR) of 87.7% from 2023 to 2030, which reflects its increasing adoption across sectors such as finance, healthcare, and supply chain.

Source: grandviewresearch.com

- BaaS platforms, offered by providers like Microsoft Azure and Amazon Web Services, simplify blockchain adoption by providing pre-built frameworks. This trend is expected to accelerate blockchain integration for businesses without in-house expertise.

- AI combined with blockchain improves data analysis and decision-making. This synergy is being adopted in supply chains, healthcare, and finance as it provides predictive analytics and secure data storage.

- The demand for cross-chain interoperability is growing. Projects like Polkadot and Cosmos enable seamless communication between different blockchains, addressing fragmentation and fostering collaborative ecosystems.

- Energy-efficient consensus mechanisms, such as Proof of Stake (PoS), are replacing energy-intensive systems like Proof of Work (PoW). This shift aligns blockchain with global sustainability goals, appealing to environmentally conscious businesses.

Whether it streamlines operations or creates secure systems, the ability to build blockchain apps that address specific industry needs has become a driver of innovation. Organizations adopt these advancements to position themselves at the forefront of this transformative era.

Conclusion

As blockchain technology continues to evolve, businesses that invest in its potential are better positioned to drive growth, improve operations, and stay competitive in an increasingly digital environment. With a systematic approach, businesses can use this technology to create innovative solutions. The steps in this guide—define objectives, select the right platform, deploy your application, and maintain it—provide a clear roadmap for addressing the complexities of blockchain development. Now is the time to turn your blockchain vision into reality and revolutionize your industry.

Post Views: 43