Bitcoin’s drop below the $50k mark was the result of short-term holders losing their cool and panicking. These folks, who are newer to the game, couldn’t handle the heat and started dumping their coins at the first sign of trouble.

The irony? Bitcoin’s dominance in the market is stronger than ever, but the actions of these jittery traders created unnecessary chaos. Glassnode data shows that since November 2022, Bitcoin has climbed its way from a 38% market share to 56%.

Meanwhile, Ethereum, stablecoins, and altcoins have seen their shares shrink. Ethereum’s share slipped from 16.8% to 15.2%, while stablecoins plummeted from 17.3% to 7.4%. Altcoins didn’t fare much better, dropping from 27.2% to 21.3%.

Capital inflows and market changes

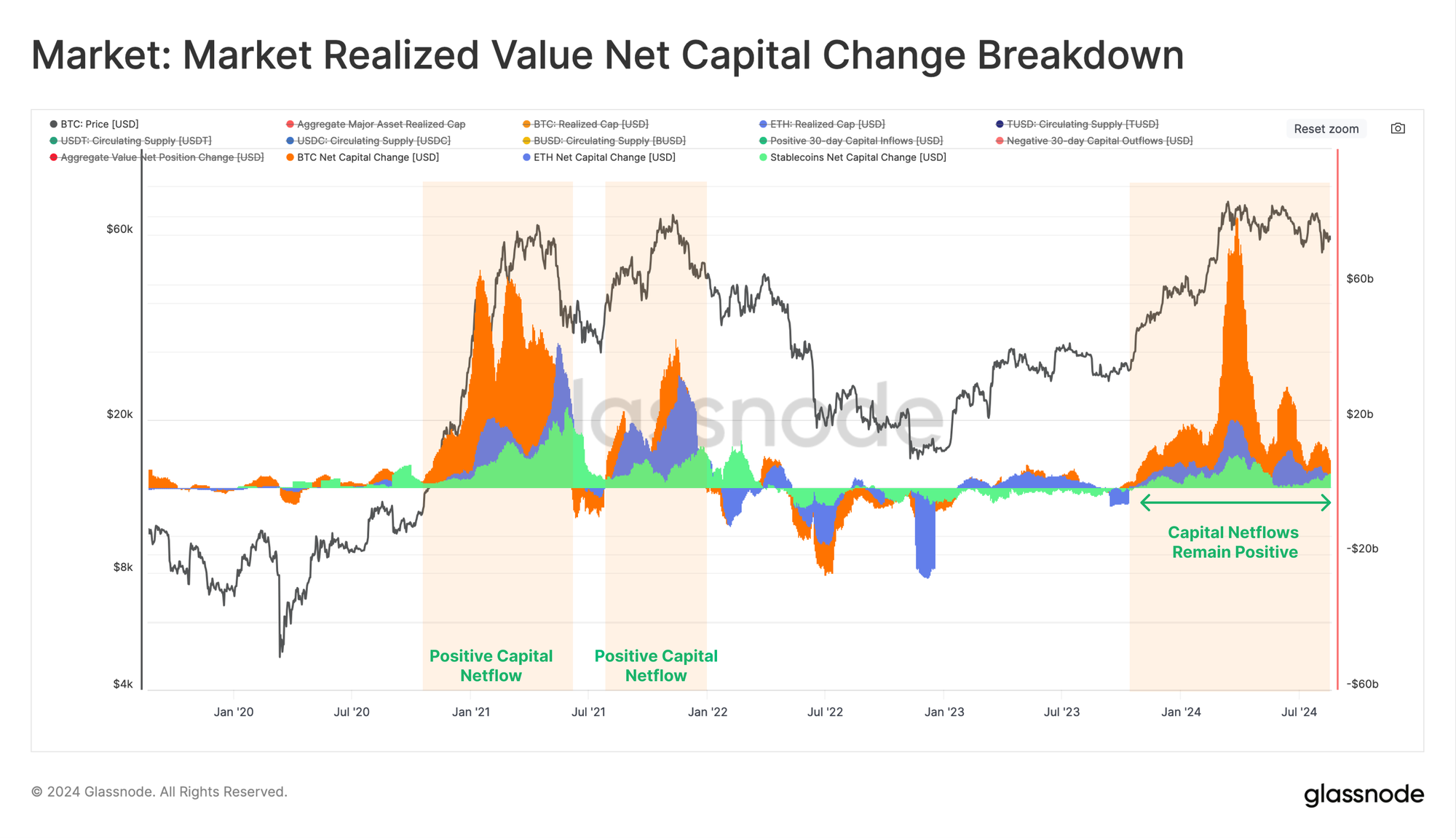

Let’s break it down. Capital keeps flowing into Bitcoin, Ethereum, and stablecoins, even though the market has generally shrunk since March’s ATH. Only about a third of the trading days saw more money coming in than usual, but that’s still a decent sign.

What’s interesting is the shift in buy-side versus sell-side metrics. These numbers tell us where the money is moving, whether people are buying more stablecoins or selling off their Bitcoin and Ethereum.

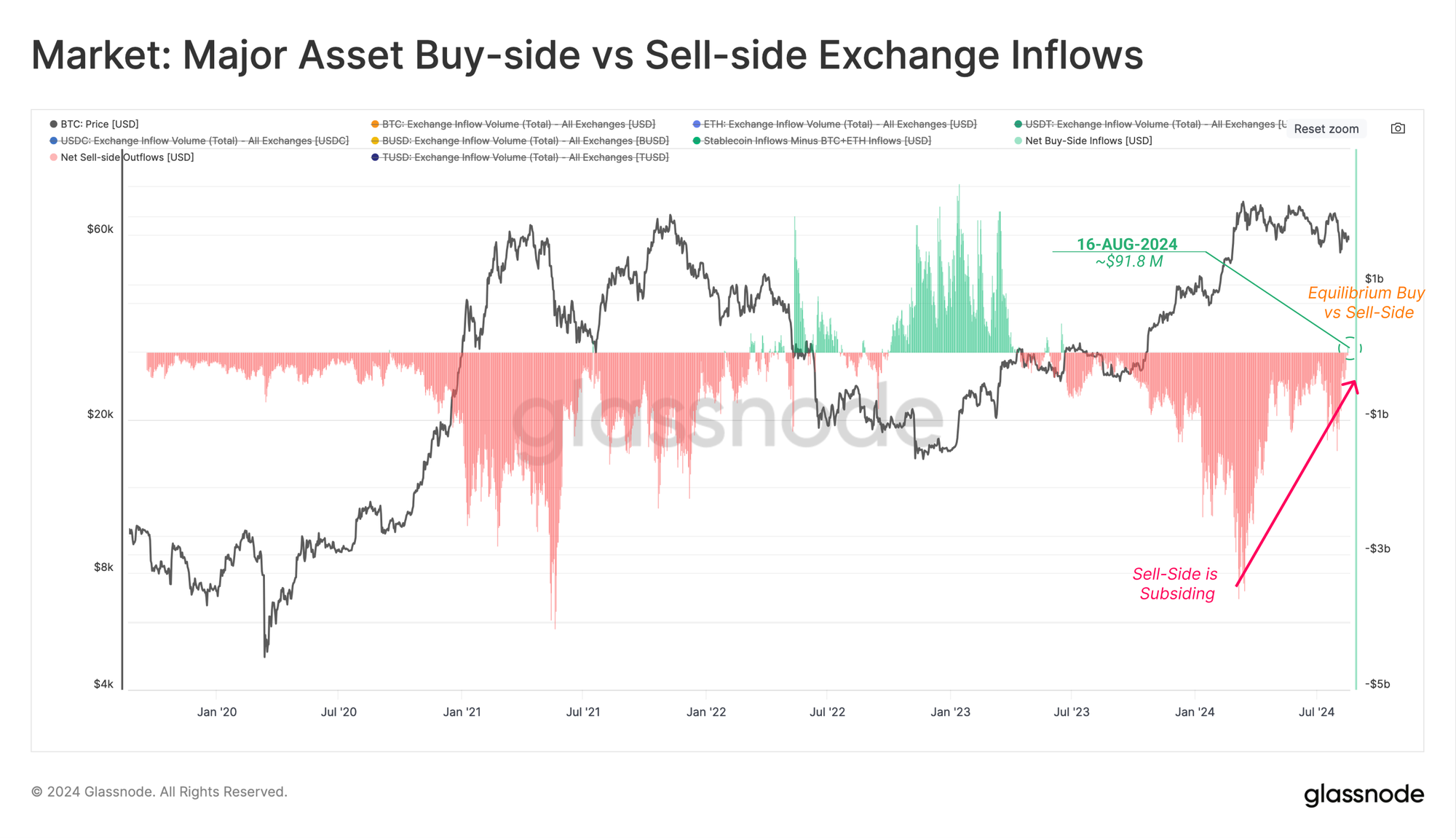

When the market hit that ATH, the pressure to sell started to ease. For the first time since June 2023, we saw some bullish movement, with a net inflow of around $91.8 million per day. But the damage was already done by short-term holders, who got spooked and started offloading their assets.

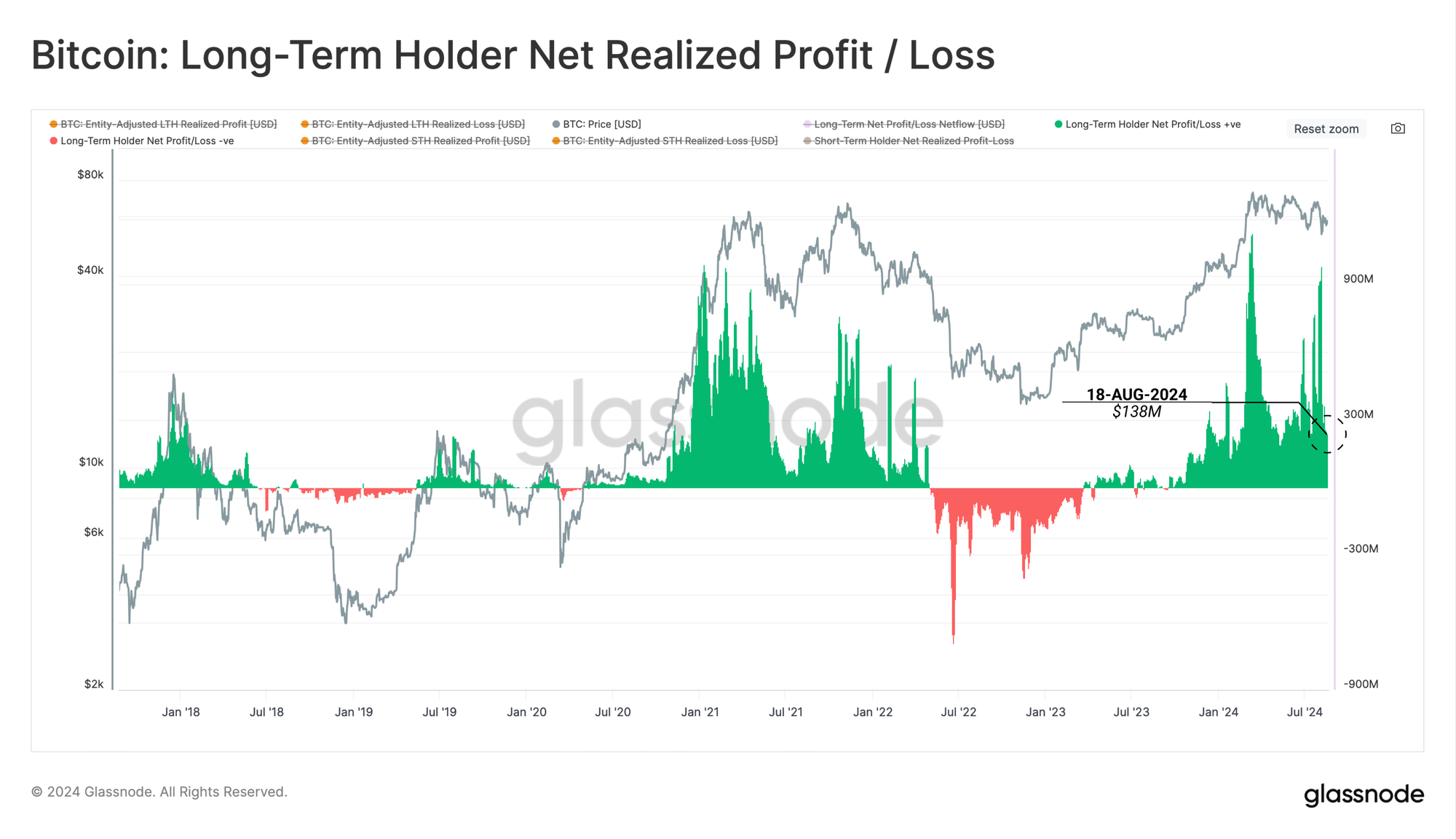

Glassnode says this overreaction is a textbook case of why these holders need to chill out. Long-term holders, on the other hand, have been making bank.

They’ve been cashing in at a steady rate of $138 million in profit every day, balancing out the supply and demand. This has kept the market from totally collapsing, but it’s also kept prices relatively flat.

The market’s behavior

When you look at the Realized Profit/Loss Ratio for long-term holders, you see that they’re still doing alright, even if they’ve started to slow down on the profit-taking.

During the ATH, this metric was through the roof, similar to what we saw in previous market peaks like 2013 and 2021. It’s cooled off now, which is good because it means we’re not headed straight into a bear market like in 2017-2018 when everything went to hell.

Long-term holders are still sitting pretty, with an average profit margin of around 75%. Their spending has slowed down, which means they’re holding onto their coins instead of selling them off in a panic.

This HODLing behavior is a big deal because it shows that these investors believe in Bitcoin’s long-term value.

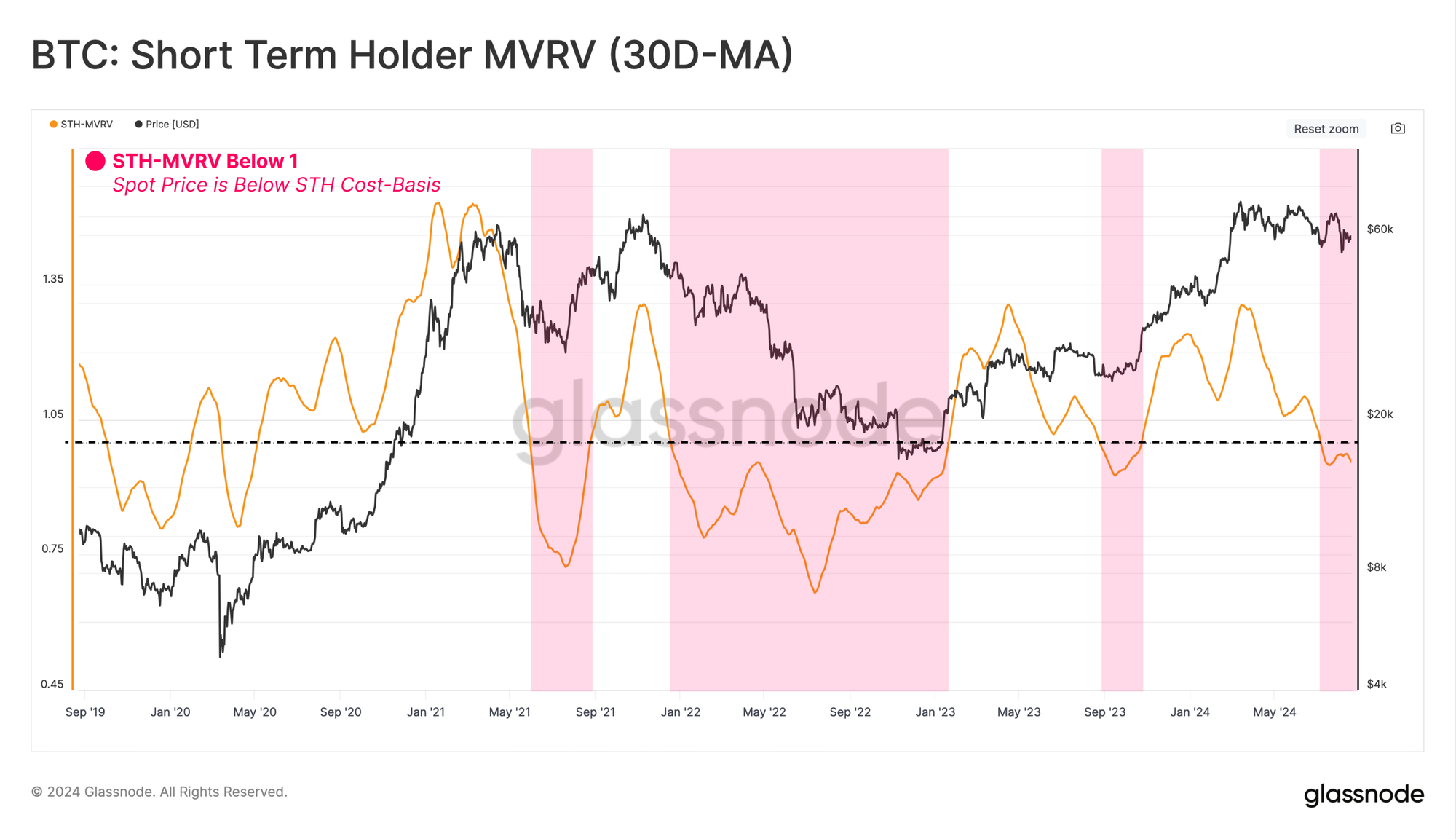

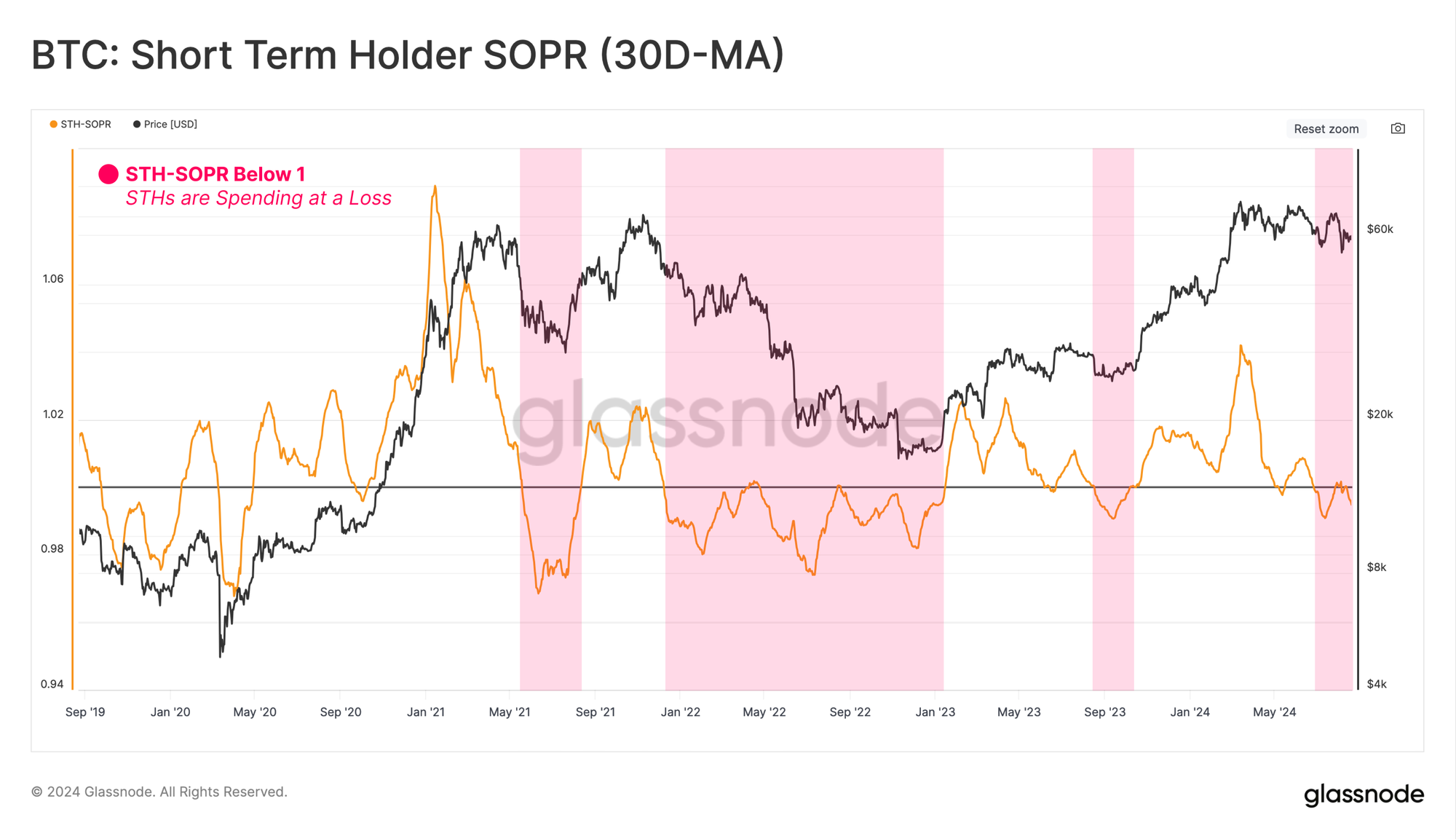

The short-term holders are feeling the heat right now. The Short-Term Holder Market Value to Realized Value (STH-MVRV) ratio has dipped below 1.0, meaning most of these recent buyers are sitting on losses.

Normally, during a bull market, you’d expect a brief dip like this, but if it drags on, it can trigger full-on panic selling. And that’s exactly what we’ve been seeing.

The expectation of a sell-off grows as these short-term holders start realizing their losses. The Spent Output Profit Ratio (STH-SOPR) for this group has also dipped below 1.0, confirming that a lot of these coins are being sold at a loss.

This creates a feedback loop, where the more they sell, the more prices drop, leading to even more panic selling.