as the 61st Project on Launchpool • crypto.ro")

The crypto market now has the highest stablecoin liquidity in its history after Tether’s (USDT) latest token issuance. This year, the supply of different types of fiat-pegged tokens increased, leading it to finally break its all-time high.

The recent Bitcoin (BTC) all-time high on November 12 followed a record series of new Tether (USDT) inflows. USDT added billions to its supply, while the value of all stablecoins surpassed peak levels from the 2021-2022 bull market.

Pegged token growth closely tied to bull runs

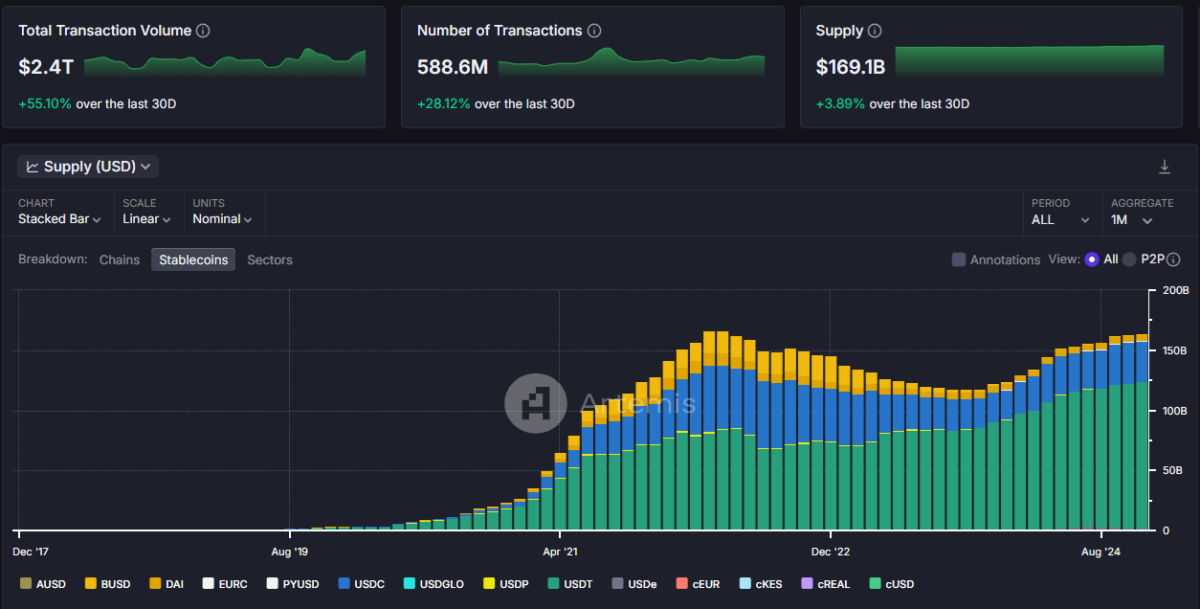

Based on Artemis data tracking a basket of 14 stablecoins, the supply expanded to 166.7B, breaking the 2022 record of 166.4B. Of that supply, a total of 125.2B belongs to USDT, after the latest addition of more than 4B tokens within a week.

Stablecoin growth, especially in the short term, remains closely tied to the biggest bull rallies, as most of the newly issued fiat-pegged tokens flowed directly into centralized exchanges.

The data was a snapshot during peak trading activity, so some may have since adjusted their supply downward.

In the past few months, the stablecoin supply has grown gradually. However, it had a hard time offsetting the outflows of several types of stablecoins. The 2024 stablecoin profile is showing marked differences, after removing more than 9B tokens of Terra’s UST, slashing the supply of DAI in half, and adding new types like Ethena’s USDe.

Bull market split stablecoins by niche

The 2024 bull market had an insatiable appetite for stablecoins as a settlement asset. For that task, the most suitable assets were USDT, Circle USD (USDC), and First Digital USD (FDUSD). Those tokens had the largest cumulative trading volumes, though skewed toward USDT.

In the past few days, USDT also achieved peak trading volumes, ranging between $240B and $263B in 24 hours. The growing demand for using USDT led to additional prints, which were absorbed into the daily turnover.

The most useful version of USDT remains the Ethereum-based ERC-20 token, with the highest share of the supply and the broadest ecosystem. These tokens are also flowing into L2s, with accelerated deposits to Arbitrum (ARB). The Arbitrum chain now carries $4.8B in stablecoin liquidity, pointing to a highly active DeFi sector.

USDC and FDUSD together reached volumes of $33B in 24 hours, though targeted to specific trading pairs. FDUSD has a volume to market cap ratio of 653%, reflecting the activity on its most widely used Binance trading pair. Even with a supply of just 2.3B, FDUSD is one of the key mechanisms for settling BTC trading on Binance.

The second tier of stablecoins tied to the 2024 bull market belong to DeFi – DAI, Sky Dollar, USDe by Ethena, and GHO by Aave. The supply of DAI fell to 3.2B, though compensated by a switch to the new asset, Sky Dollar.

The supply of USDS stabilized at 5.12B, leaving Sky/Maker with more than 8.3B in pegged token value. The Sky/Maker ecosystem is much closer to its peak value at 9.8B tokens, achieved in February 2022.

GHO, the stablecoin issued by Aave, expanded its supply to 180M tokens, with the goal of serving the Aave ecosystem. GHO also spread to other DeFi protocols and gained prominence above other algorithmic stablecoins.

The remainder of the supply is made up of less active asset-backed tokens, including Gemini USD (GUSD), the almost phased-out Binance USD (BUSD), and other regulated tokens like PayPal USD (PYUSD).

The remainder of the stablecoin market is for niche tokens with under $100M in value locked. Those tokens are riskier. Some fail to hold at the $1 peg, while others serve only one protocol. A total of 119 different tokens emerged over the past few years, copying the models of larger projects.